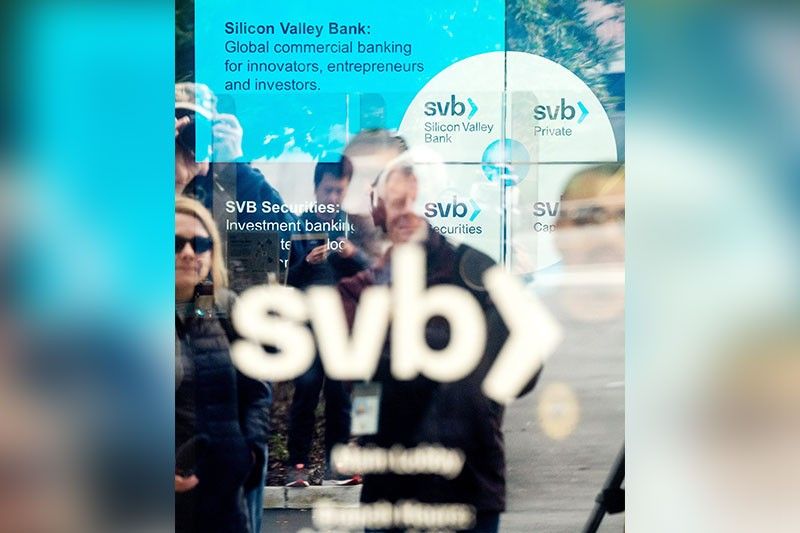

Bank shares rebound on SVB sale

NEW YORK, United States — Bank shares rallied to lift most major stock markets on Monday as fears of a sector crisis eased after a regional US lender took over most of collapsed rival Silicon Valley Bank.

The rebound followed a rout in bank shares on Friday over concerns that the turmoil in the sector now threatened German giant Deutsche Bank.

Both the Dow and S&P 500 advanced Monday, although the Nasdaq finished lower following a choppy session.

Shares of North Carolina-based First Citizens Bank surged more than 50 percent after US regulators announced that it was taking over much of SVB's business.

Shares in other US regional lenders also jumped, including those of San Francisco-based First Republic Bank, whose troubles have triggered efforts by Wall Street giants including JPMorgan Chase to rescue it.

In European trading, Frankfurt rose 1.1 percent, with shares in troubled Deutsche Bank gaining more than four percent after diving by 8.5 percent on Friday.

London and Paris stock markets also rose, with British lender Barclays and French peer BNP Paribas climbing more than 2.5 percent.

'Anxiety to remain'

The US Federal Deposit Insurance Corporation (FDIC) announced late Sunday that First Citizens agreed to buy the deposits and loans of SVB, whose collapse this month had sparked fears of a global contagion.

The news helped "lift sentiment across the banking sector after a rocky end to last week, though the pall of banking stress still hangs over the market," said analyst Neil Wilson at trading firm Finalto.

But International Monetary Fund chief Kristalina Georgieva on Sunday warned that risks to financial stability had increased -- and stressed "the need for vigilance" following the turmoil.

On Monday, the World Bank warned that an anticipated economic slow-down in China is likely to drag global growth down to its lowest level this century as it proposed measures to prevent a "lost decade" of growth.

Concerns over Deutsche Bank rocked markets last Friday, particularly after contagion fears led to the Swiss government-engineered takeover of troubled Credit Suisse by domestic rival UBS.

"Anxiety is going to remain until we have a few weeks of calm and despite the small frenzy on Friday, I think we can say that the first of those is now behind us," said Craig Erlam, senior market analyst at OANDA trading platform.

'No bank is immune'

Clifford Bennett, chief economist at ACY Securities, said it was unlikely the German government would allow Deutsche Bank to collapse or face restructuring but it showed the growing pressure on the banking system.

"No bank is immune in the current climate. The forces that lead to the crisis so far seen, of higher rates and depositor uncertainty, only continue to grow," he wrote in a note.

Deutsche Bank returned to financial health last year following a major restructuring after years of problems, but its shares sank last week after the cost of insuring against the bank defaulting on its debt spiked.

Markets had rallied earlier last week after authorities took measures to shore up the banking sector, but sentiment soured by Friday after a raft of central bank rate hikes in the United States and Europe.

In Asia on Monday, Hong Kong and Shanghai stocks fell, while Tokyo, Sydney and Singapore rose.

Elsewhere, oil prices pushed higher, with US benchmark West Texas Intermediate piling on more than five percent in part due to technical trading factors.

- Latest

- Trending