Medilines Distributors is just the worst in a recent pack of pretty ugly IPOs

One look at the IPO Tracker is enough to see that the last four months of IPOs is just filled with red.

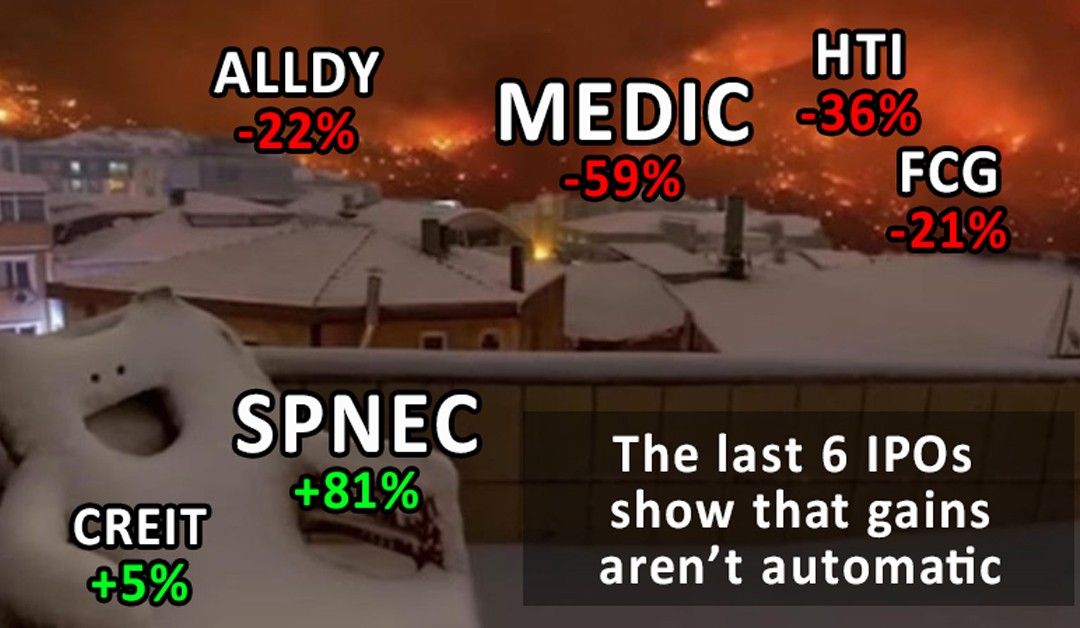

Sure, the first-day performance has been fine; the only outright first-day tragedy was Medilines Distributors' [MEDIC 0.94 1.05%] first-day horror-show.

But of the six IPOs that we’ve had since the end of Q3, only two are trading above their IPO price: Solar Philippines NEC [SPNEC 1.81 2.16%], and Citicore Energy REIT [CREIT 2.69 0.37%].

The rest are all swimming in a sea of red. Manny Villar’s AllDay Marts [ALLDY 0.47 2.08%] started its life hitting the ceiling in what PNB Capital (the underwriter) called “overwhelming demand”.

Manny Villar himself said that the brisk uptake of the shares “validates this price”. It was oversold going into the IPO and had a stabilization fund.

Since the IPO, however, the stock is down over 21%. MEDIC was next, and we all should remember how that went: terribly, from the very beginning, to the very... now. It had an oversubscribed institutional tranche and no stabilization fund.

It’s currently down 59%. After that, SPNEC was born, and it’s done very well for itself.

No problems. Oversubscribed with no stabilization fund.

It's up 81%. After SPNEC, though, came Haus Talk [HTI 0.96]. Possibly oversubscribed. No stabilization fund.

Despite a strong real estate market and voluminous demand for lower- and middle-income housing, HTI is currently down a brutal 36%. Next came Figaro Coffee [FCG 0.59 1.67%], which is actually Angel’s Pizza, which is actually just a Cirtek [TECH 3.36 1.18%] sister company.

It wasn’t oversubscribed, but it did have a stabilization fund.

The last IPO, CREIT, was oversubscribed and had a stabilization fund, and finished its first day up 11%. It’s now at +5% after a recent rough ride for REITs.

MB BOTTOM-LINE

If there’s a takeaway to be had, it’s that IPOs are not guarantees of anything. It’s possible to take a good business with strong prospects, get an oversubscribed IPO offer period, and still watch in horror as the stock tanks on the IPO day or after the stability fund expires.

I don’t mean to say that what happens with IPOs is necessarily random, but I think that it’s important for all IPO investors to consider “the other side” when consuming the IPO company’s promotional materials (and yes, a prospectus should be considered promotional material).

On the topic of expectations, I think it’s also important to talk for a second about stabilization funds.

They provide some downside protection, though it is important to remember that the protection provided from a stability fund is not absolute. Remember the IPO of AREIT [AREIT 47.40 4.05%]?

It had a stability fund, but the downward selling pressure on the stock was so hard that the stabilization agent couldn’t keep the price from dipping below the IPO offer price, where it stayed for nearly two months before going on an epic rip.

Another limitation of the stability fund is time, as it is only active for the first month, or until the quota of stock has been exhausted.

After that point, the stock is on its own. Unless there is significant organic demand for the stock, the post-stability fund price will probably drop.

This was most recently seen with FCG, where the stock price remained above the IPO offer for the entire lifespan of the stability fund, and dipped below the offer price (P0.75/share) basically the day after the fund expired.

The price has never recovered and is currently down more than 20% from the offer price, and down more than 35% from its post-IPO high of P0.92/share.

I don’t say any of this to imply that Bank of Commerce’s [BNCOM 12.00 pre-IPO] stability fund (or any other stability fund for that matter) won’t be sufficient, or that the price will drop below offer once the fund expires; I bring it up only to adjust investor expectations about what a stability fund can do and what it can’t do.

Don’t get me wrong: a stability fund is a great thing to have, and in a weak market or shaky offering, it can be a great source of liquidity for nervous IPO buyers looking to get out if things don’t immediately go super great.

--

Merkado Barkada's opinions are provided for informational purposes only, and should not be considered a recommendation to buy or sell any particular stock. These daily articles are not updated with new information, so each investor must do his or her own due diligence before trading, as the facts and figures in each particular article may have changed.

- Latest