The almighty US dollar falls

Last year, the US dollar took a long and sustained nosedive that sent the currency slumping to its lowest level in three years. The US dollar index (DXY) – which measures the value of the US dollar relative to a basket of foreign currencies belonging to the US’ biggest trade partners – lost nearly 10 percent, registering its biggest yearly loss since 2003.

About-face baffles analysts

The dollar’s abrupt and complete reversal at the start of 2017 surprised most analysts who earlier were forecasting a stronger US dollar for the year. Analysts were expecting a stronger US dollar given the following reasons:

1) Expectations of higher US interest rates

2) Stronger US economic growth

3) Rising corporate earnings

4) Passage of the tax reform in the US

5) Inflow of portfolio investment due to the bull market in US stocks

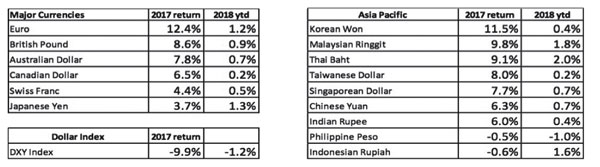

2017 performance of major and Asian currencies vs. the US dollar

Source: Wealth Securities Research

Dollar weakens against most currencies

The dollar was weak against almost all currencies in 2017. The euro was the best performer among major currencies, gaining 12.4 percent and hitting its highest level in three years. The British pound and the Aussie dollar followed next with gains of 8.6 percent and 7.8 percent, respectively.

In Asia, the Korean won strengthened the most against the dollar, up 11.5 percent for 2017. The Korean won closed at its highest level against the US dollar in more than three years. This was followed by the Malaysian ringgit and the Thai baht which appreciated 9.8 percent and 9.1 percent against the greenback, respectively.

The US dollar index, which is a weighted basket of major world currencies such as the euro, Japanese yen, Canadian dollar, British pound, Swedish Krona and Swiss Franc was down 9.9 percent.

Currency performance year-to-date

As shown in the table above, dollar weakness persists in 2018. The DXY is down 1.2 percent year-to-date. The yen has strengthened 1.3 percent. The euro is at new three-year highs and is up 1.2 percent year-to-date. Asian currencies are up an average of 0.8 percent, led by the Thai baht and the Malaysian ringgit which are up two percent and 1.8 percent, respectively.

Central bank policies and their effect on global currencies

In recent years, central bank policies have dictated the movement of global currencies. In our book Opportunity of a Lifetime and in numerous Philequity Corner articles, we discussed extensively how coordinated central bank action was able to stave off a double-dip global recession and deflation. By implementing zero interest rates and unconventional monetary policies, global central banks started the Great Global Monetary Easing (see The Great Global Monetary Easing, Oct. 22, 2012) to achieve economic stability and growth.

With the Fed ahead of the curve, the US economy was the first to recover. And in 2014 when the Fed was already ending its QE program, other central banks were still pursuing a turnaround in their respective economies. This policy divergence fueled the sharp appreciation of the US dollar in 2014 to 2016 with the DXY rising as much as 30 percent over the period.

Synchronized global economic growth

By 2017, it was clear that the coordinated central bank action of unprecedented monetary stimulus in previous years had paid off and resulted into synchronized growth around the globe. This time around, it was not only the US economy, but the economies of Europe, China and Japan which showed improving and sustainable economic growth.

ECB and BOJ on the path to normalization

With Europe and Japan back on solid economic footing, the ECB and the BOJ started tapering their own QE program since last year. In April 2017, The ECB announced it was reducing its monthly asset purchases from 80 billion euros to 60 billion. Last October 2017, it announced a further reduction to 30 billion euros. Similarly, the data from the BOJ show asset purchases fell 52 percent in 2017. BOJ showed assets in their balance sheet grew by only ¥44.9 trillion in 2017, compared to a ¥96.4 trillion increase in 2016.

Currency diversification

Expectations that the ECB, BOJ and other central banks would normalize their respective monetary policies have caused investors to rush into the euro, the yen, as well as most other currencies that have suffered from excessive weakness in previous years.

What is clear is that we are experiencing synchronized global economic growth which affords other central banks to modify their ultra-accommodative monetary policy stance. Expectations that other central banks will soon start raising benchmark rates have led investors to diversify their currency holdings.

Emphasis on country fundamentals

The direction of the US dollar will continue to have a bearing on how global currencies perform. But this time around, we expect increasing emphasis on the each country’s fundamentals, especially the monetary and fiscal policies. Factors that “traditionally” determine exchange rate movements such as the current account, balance of payments, fiscal account, interest rates, inflation rate, political stability and economic (GDP) growth will be given more importance.

Philequity Management is the fund manager of the leading mutual funds in the Philippines. Visit www.philequity.net to learn more about Philequity’s managed funds or to view previous articles. For inquiries or to send feedback, please call (02) 689-8080 or email [email protected].

- Latest

- Trending