A student asks about buying a VUL

Question from a reader: Hi Ms. Rose. I just wanted to send you a message to tell you that you are such an influential woman and I really look up to you. You have contributed a lot to my growth, especially in handling my finances. I would like to ask if you have plans of conducting seminars, because I’d love to attend one. May I also ask what you think about me buying a VUL? I’m still a student and graduating soon. I already built my emergency fund and my next step is to get myself insured and to invest. Would you recommend buying a VUL for me? God bless you even more and keep on inspiring us. ![]() – Isabel via FB page PM

– Isabel via FB page PM

My answer:

Thank you for your kind words Isabel. And congratulations for having already built your emergency fund while still a student! Big cheers to that. It makes me feel great to know that a young student has immediately implemented an FQ lesson learned.

Regarding the seminar, we are set to have one by the end of the year, so I hope you can join us there. I will be posting the details once finalized.

On the matter of the VUL, I think I have also received and answered similar questions on this in my previous articles. There was one asking what to do with her husband’s VUL and another one asking if she should buy her minor child one. Add to that the talks and guestings where I’ve discussed the matter. Each time I give my take on this, I always got some “hater comments” so I wouldn’t be surprised if I’ll receive some again today. ![]()

VUL stands for Variable Unit-Linked Investment or Variable Universal Life Insurance. It is a permanent life insurance with built-in savings/investment component. You mention that after your emergency fund, your next step is to get yourself insured and start investing. Naturally, a 2-in-1 looks very attractive to you. But let’s take a closer look.

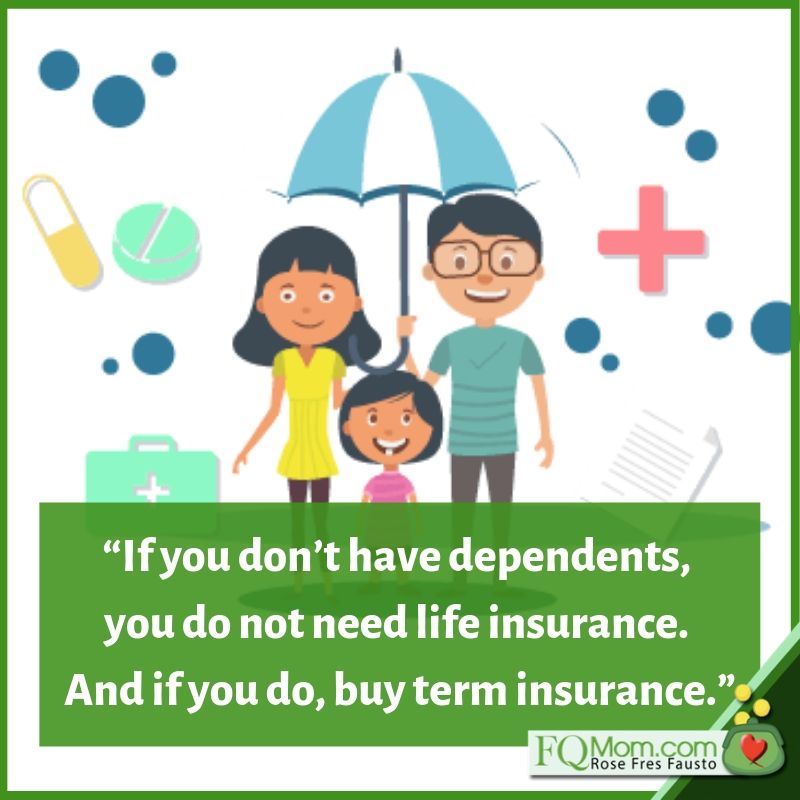

First question: Why do you want to get insured? Are you the family breadwinner? Do you have dependents? You see, life insurance is a financial product that a prudent person should buy in order to protect her dependents in the event of an untimely death. When you die, will there be people whose lives will be financially crippled because of the loss of your financial contribution? I’m assuming you don’t have dependents at this point in your life; otherwise, you would have mentioned it. The simple rule is: If you don’t have dependents, you do not need life insurance. If you hear someone say, “It’s better for you to buy insurance now that you’re still young because it’s cheaper,” just refer that person to the simple rule in bold letters. Even a 99% discount is “more expensive” than zero.

Just in case you do have dependents, the cheapest way to insure yourself is by buying term insurance.

For rough illustration purposes, a one million coverage will cost you around P5,000 premium payment per year compared to a VUL of over P25,000 per year, depending on age, and other factors. Of course, the reason for the higher cost of the latter is the investment portion.

This leads us to the second question: How is the investment feature of the VUL? Let’s check. For the first three or so years, your premium payments primarily go to the insurance, commission and other administrative costs. Again, roughly, for illustration purposes, out of the P25,000 annual premium you pay, only about P5,000 goes to your investment. This is the reason why a lot of those who buy this investment instrument are surprised to find out that after the first few years of paying, their investment value is oftentimes even lower than their actual contributions. Nagkakagulatan! But then the option of withdrawing or stopping the plan is heavy on the heart because of the sunk cost fallacy. (To read more on this, click here) To get the exact figures, you may ask your insurance agent to give you sample computations based on your personal circumstances – age, health condition, etc.

Why are VULs and similar “tisoy instruments” the bestsellers?

Here’s a tidbit of insurance history. All insurance products used to be term in nature. But there was a clamor from policyholders who became upset with the thought that after paying their premiums for 20 to 30 years, they have nothing tangible in terms of cash accumulation. Take note that the insurable age for term insurance is usually up to 85 years. So, if you live beyond that, you may feel that you don’t have anything to show for all the decades of payments. And that’s why insurance companies came up with products with cash values, against which the insured can even borrow.

The VUL and similar combo or tisoy types of insurance became very appealing and lucrative to the companies and insurance agents, and that’s why for every visit that you get from an agent, this is always on top of their marketing pitch.

The idea of having a 2-in-1 is very appealing and simple to the one who’s buying. “Insured ka na, may investment ka pa!” They also like the idea of having an assured value somewhere which may not be found in other investment instruments.

Couple that with the pleasant and patient encounter with an insurance agent versus bank staff who sometimes even discourage you to buy UITF either because they don’t quite understand it or they would rather have your cash in their traditional savings and current accounts and time deposits.

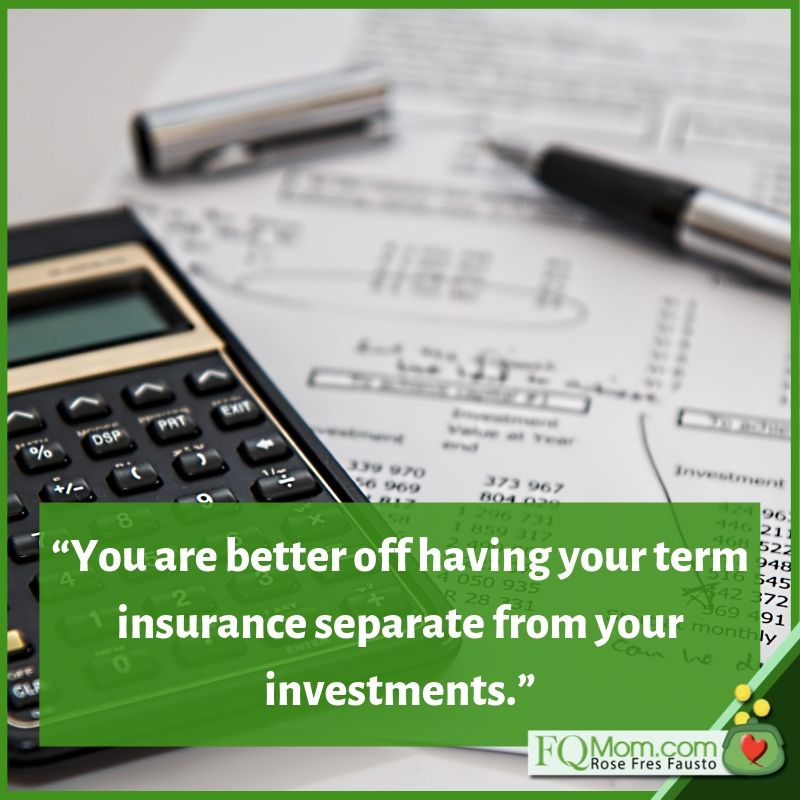

For your purposes, you are better off investing in index funds – either UITF (Unit Investment Trust Funds) from banks or mutual funds from fund houses or through online platforms like COL Financial where you can buy almost all mutual funds in the country. If you’re just starting off your life-long investment journey, I suggest that the underlying asset of your index funds be equity because this is the asset class that gives the highest returns in the long run. But if you have shorter term uses for the money, then you can have a combination of fixed income and equity.

Do your investing regularly and the best way to do it is to automate it. And when the time comes when you’d need both insurance and investment, have them separately. Buy your term insurance up to the amount that you need, and continue investing regularly in funds that give you the appropriate risk-return for your goals.

That’s true, I think the only time I will buy a VUL or other similar tisoy insurance/investment product (the way they are structured right now) is when my own child or grandchild is in a life-changing competition of selling the most number of this product. Then I’ll also ask him/her to share the commission with me, hahaha! ![]()

Kidding aside, I think I’m still very Filipino (i.e. tame) in explaining why you are better off not buying a VUL. If you want to see how the finance gurus in the US give their bombastic explanations, here are a couple of short videos you may wish to watch. ![]()

Cheers to high FQ!

*********************************

ANNOUNCEMENTS

1. MOM AND SON PODCAST – SEASON 3 EPISODE 9 (TRAVEL TIPS)

How do you make the most out of every peso you spend when you travel? People say that traveling is something you spend on that actually makes you richer. What does this mean? Join us as we discuss some of our FQ tips when it comes to traveling and why we believe it is an important activity to save up for and practice wisely!

#MomAndSonPodcast

Stream the episode now using these links:

Spotify

https://open.spotify.com/episode/7IwjxZK1CSwUx7Ozrfhabn?si=4o7BQLrVRFanQkTIBYgC5Q

Apple iTunes

https://podcasts.apple.com/ph/podcast/mom-and-son-podcast/id1449688689?mt=2

Google Podcasts

https://podcasts.google.com/?feed=aHR0cHM6Ly9mZWVkcy5idXp6c3Byb3V0LmNvbS8yNDE0NDcucnNz

Buzzsprout

https://www.buzzsprout.com/241447/1603387-mom-and-son-podcast-season-3-episode-9-travel-tips

YouTube:

(originally uploaded in Anton Fausto’s YouTube channel: https://youtu.be/yEyYnP1GXu4)

FQ Mom’s YouTube channel: https://youtu.be/ZRY4C9mXSYw

2. Thanks to those who already bought the FQ Book, especially to those who took the time out to send me their feedback. Your feedback is food for my soul. To those who have not gotten their copy yet, here’s a short preview of FQ: The nth Intelligence

You may now purchase the book in major bookstores, or if you want autographed copies, please go to FQ Mom FB page (click SHOP), or FQMom.com (click BOOKS), or email us at FQMomm@gmail.com

Rose Fres Fausto is a speaker and author of bestselling books Raising Pinoy Boys and The Retelling of The Richest Man in Babylon (English and Filipino versions). Click this link to read samples – Books of FQ Mom. She is a Behavioral Economist, Certified Gallup Strengths Coach and the grand prize winner of the first Sinag Financial Literacy Digital Journalism Awards. Follow her on Facebook&YouTube as FQ Mom, and Twitter&Instagram as theFQMom. Her latest book is FQ: The nth Intelligence.

IMAGES ATTRIBUTION: Photos from photos.com by Getty Images (AndreaObzerova), bankbazaarinsurance.com, and canva.com,modified and used to help deliver the message of the article.