Is the bear back in emerging markets?

In our previous article, we discussed the stark contrast between the performance of US stocks and international stocks (USA vs. the world, Sept 3. US stocks have performed well year-to-date as the Dow, S&P 500, Nasdaq and Russell are trading near their all-time highs. However, most other global markets are consolidating or correcting, with many countries hovering on bear market territory.

USA soars, international stocks languish

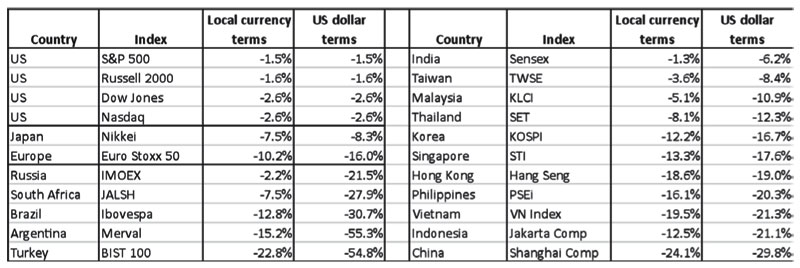

In the table below, we show that US indices are within three percent from their record highs. In contrast, emerging countries such as Argentina, Turkey, Brazil, South Africa, China and Indonesia are in bear territory after dropping more than 20 percent in US dollar terms. The PSEi is down 16 percent from its all-time high of 9,079. However, measured in US dollar terms, the PSEi is now in bear territory as it is down 20 percent from the peak.

Performance of various indices – drawdown from the peak

Sources: Bloomberg, Wealth Research

Sources: Bloomberg, Wealth Research

Trouble in emerging markets

The ongoing correction in EM stocks was triggered by specific problems that each EM country is facing. Turkey and Argentina are in the midst of a severe economic and financial crisis. China, the world’s biggest emerging market, is weighed down by the possible consequences of a trade war and decelerating economic growth. South Africa recently entered a recession and Indonesia is saddled by a weakening currency and widening deficits. Meanwhile, the Philippines is troubled by fast-rising inflation, a weaker peso and twin deficits on our current account and government budget.

As such, the currencies of troubled EM countries have sharply depreciated this year. For example, the Argentinian peso plunged by a staggering 98 percent while the Turkish lira sank 69 percent year-to-date. Other currencies which dropped sharply year-to-date are the South African Rand (-23 percent), Brazilian real (-22 percent), Russian ruble (-21 percent), Indian rupee (-12 percent) and Indonesian rupiah (-9 percent). Tracking the movement of the EM currencies, the Philippine peso declined by eight percent year-to-date.

Correction or bear market?

EM stocks dropped sharply this year due to the US-China trade war and fears of contagion as the macroeconomic fundamentals of certain EM countries have markedly deteriorated. Considering this, market pundits have commented that the EM basket is already in bear market territory. Despite the steep correction in EM stocks, current market conditions are still far from what we experienced in the 1997 Asian financial crisis and 2008 subprime mortgage crisis. Currently, there is no broad-based economic recession or credit crisis around the globe.

Corrections – long or short?

In our investor briefing last Sept. 1, we received questions about the heightened volatility and recent weakness of the market. We explained that pullbacks are part and parcel of the stock market. We also said that it is extremely hard to predict the timing, magnitude and duration of market drawdowns. Nonetheless, we referred to statistics and historical data to analyze significant pullbacks in the past. In the US, the average correction (excluding bear markets) is a 13 percent drawdown from the peak. On average, it takes four months for prices to move from peak to trough. Incidentally, the average recovery period (or the move from trough to peak) is also four months.

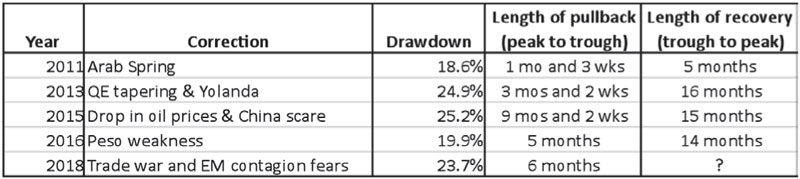

Phl corrections during this bull market

The PSEi is now down 20 percent in US dollar terms from its all-time high of 9,079. Our market’s sharp drawdown has prompted many to ask if the PSEi has already entered a bear market. It is worth noting, however, that drawdowns of -20 percent or more are not rare in the context of a long bull market. As we showed in our investor briefing and as seen in the table below, the PSEi has experienced four significant pullbacks in the current bull market before recovering to new all-time highs.

Significant corrections of the PSEi since 2009

Sources: Bloomberg, Wealth Research

A vigilant BSP

Last week, the government reported that inflation in August reached 6.4 percent. This came above most forecasts and is the highest reading since March 2009. In response, the BSP announced that it would be steadfast and act strongly to arrest rising inflation. Going forward, it will be important for the BSP to remain even more vigilant against higher inflation in this difficult environment for emerging markets. In this light, maintaining the stability of the peso is crucial in taming the impact of imported inflation.

A challenge for the government

Our country is experiencing a steep rise in prices mainly due to supply-side problems, higher oil prices and a weakening currency. These developments are taking place amid a challenging global environment for emerging countries. In this light, it is imperative for the government to be proactive and decisive in addressing the inflation problem to prevent it from spiraling out of control.

Philequity Management is the fund manager of the leading mutual funds in the Philippines. Visit www.philequity.net to learn more about Philequity’s managed funds or to view previous articles. For inquiries or to send feedback, please call (02) 689-8080 or email [email protected].

- Latest

- Trending