Surging dollar, slumping euro

The euro slipped to a new 12-year low against the US dollar last week as investors bet on the normalization in US monetary policy ahead of the Fed’s policy meeting this week.

The euro fell to an intraday low of 1.0462 last Friday, its lowest point since January 2003, before recovering to 1.0496, 1.11 percent lower on the day. Meanwhile, the US dollar index which compares the greenback against a basket of widely traded currencies, resumed its ascent by gaining 0.98 percent to 100.18, its highest level since December 2002.

Longest & sharpest decline in euro history

The recent slump in the euro is the longest and sharpest in its entire history (since its birth in 1999). The beleaguered currency has lost around 25 percent of its value against the US dollar since July 2014. It is also on its way to recording its 9th consecutive monthly loss against the greenback.

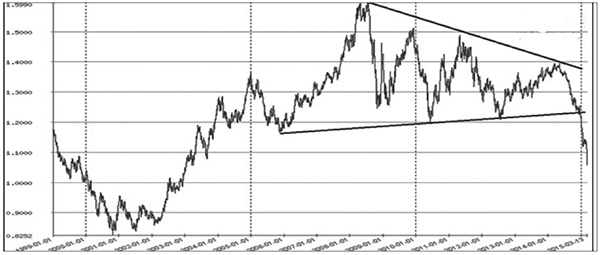

Looking at the euro’s historical chart below, the clear break below the decade-long support at 1.20 points to a medium-term target of parity against the US dollar. We see the euro testing 1.00 or parity against the US dollar, and possibly going to 0.95. Longer-term, it may even go to its all-time low of 83.95 against the US dollar.

EURUSD Weekly Chart (1999 – Present)

Source: www.fxtop.com, Wealth Securities Research

Factors weighing on the euro

A number of factors continue to weigh on the euro. Among them is the continued monetary easing as Europe tries to stave off a deflationary crisis. The inflation rate in the Euro Area was recorded at -0.30 percent in February 2015, following -0.60 percent in January 2015 and -0.2 percent in December 2014.

Adding to euro’s weakness is the ECB’s QE bond buying program. It officially started last week when the ECB bought 10 billion euro worth of bonds. The ECB has said it would buy a total of 60 billion euros worth of Eurozone government bonds a month up until September 2016.

In addition, fears of a possible Greek exit of the euro and the conflict in Ukraine are increasing uncertainty, further pressuring the euro.

Divergent central bank policies

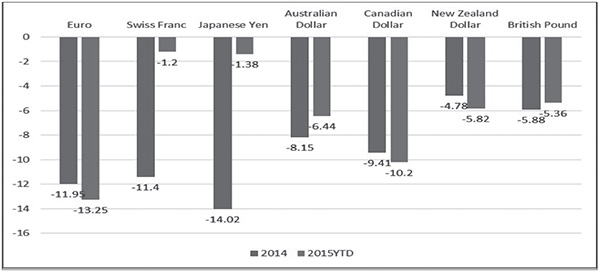

On the flipside, the US dollar has surged not only against the euro but also against most developed-market currencies as investors anticipate the Fed raising interest rates for the first time since 2006 (see chart below).

Note that since the 2nd half of 2014 the pace of US dollar appreciation has quickened as central bank policies started to diverge with the Fed leaning towards tightening while other central banks continued with their easing frenzy. Since the start of the year alone, 24 central banks have eased policy rates in one form or another.

Major Currencies vs. US dollar (% depreciation)

Source: Wealth Securities Research

Fed raising rates soon?

The recent strong US jobs data from February is widely expected to persuade the Fed to hint that a rate increase will come as early as June. Investors are wagering the removal of the word “patient” at next week’s FOMC meeting. This would then be seen as another step in the process of policy normalization and a powerful catalyst for further US dollar strength.

Peso: stable against the dollar and strong against the euro

As discussed in our article a month ago (see Philippine Peso: A Haven of Stability, Feb. 2, 2015) and as shown in our Investor Briefing last Saturday, the peso has been a haven of stability in the midst of wild swings in the currency market. The peso has been stable against the dollar while actually strengthening against the euro and most major currencies.

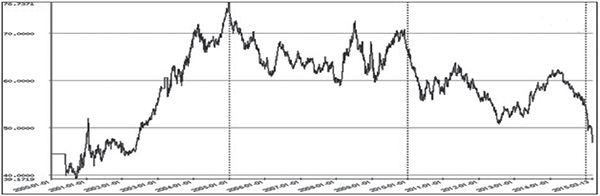

Last week, the peso rallied to 46.90 against the euro, its strongest level in 12 years. Below, the long-term EURPHP chart points to further peso strength against the euro going forward.

EURPHP Weekly Chart (2000 – Present)

Source: www.fxtop.com

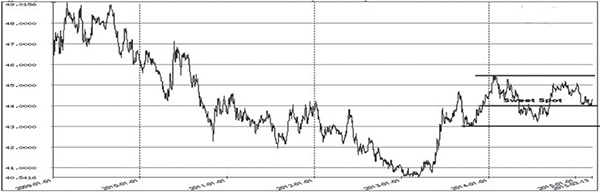

Meanwhile, the peso has remained steady against the US dollar, trading within its sweet spot of 43 -45.50 since the 2nd half of 2013. Looking at the chart below, the peso may even strengthen towards 43.50 if 44 if broken. Thereafter, it may rally towards 43 if 43.50 is breached.

USDPHP Weekly Chart (2009 – Present)

Source: www.fxtop.com, Wealth Securities Research

Peso: not too hot, not too cold, but just right

Given the dollar strength and the recent bout of currency volatility among major currencies, we are closely monitoring the potential impact on the peso. But so far, so good. Our stable peso, as well as our strong stock market (which reached new all-time highs last week), is a manifestation of the strength of the Philippine economy.

Thanks to the BSP who has successfully smoothed out excessive volatility these past years, the Philippine peso is right at its “sweet spot,” just as we have been saying these past years (see Peso’s Sweet Spot, Jan. 30, 2012, Peso Back to the Sweet Spot, June 3, 2013, The Goldilocks Peso, Nov. 4, 2013).

The peso is “not too hot, not too cold, but just right” as Goldilocks, the BSP, Philequity, investors and the Philippine economy in general, would have preferred it.

Philequity Management is the fund manager of the leading mutual funds in the Philippines. Visit www.philequity.net to learn more about Philequity’s managed funds or to view previous articles. For inquiries or to send feedback, please call (02) 689-8080 or email [email protected].

- Latest

- Trending